Quitting Smoking in 2025: A Fresh Start for the New Year

Posted 22nd January 2025 by Emily Coomer

With new year new me in full swing, quitting smoking and vaping can often be at the forefront of people’s minds, and for good reason. The benefits extend beyond personal health, having a positive impact on financial wellbeing and easing stress on the NHS too.

Let’s take a look at the benefits in some more detail:

Health & NHS

Statistics from the Office for National Statistics highlight the urgent need to quit smoking. Between 2016 and 2017, there were approximately 485,000 smoking-related hospital admissions-more than 1,300 each day. Smokers visit their GP 35% more often than non-smokers, and they face higher risks of heart attacks, lung cancer, and high blood pressure. These health issues contribute to the strain on the NHS. [1]

The Role of Vaping

While many see vaping as a “healthier” alternative it can come with its own health drawbacks, although vapes and e-cigarettes do not have tobacco in them which is the toxic substance found in cigarettes that can cause cancer. Common side effects of vaping include, coughing, mouth and throat irritation, shortness of breath and headaches [2]. Insurers also generally categorise vape users similarly to smokers which can lead to increased premiums for those who vape. It’s crucial to disclose any nicotine use to your insurance provider to avoid issues with claims.

Support for Quitting

Public Health England’s Stoptober campaign is just one free initiative that supports smokers in their quest to quit. The campaign has already assisted over 2.5 million people [3]. Successfully remaining smoke-free for 28 days can make you five times more likely to quit for good.

There are also paid seminars that smokers can attend, famously the Allen Carr’s Easyway, which Protect Line have previously partnered with, to quit smoking that has helped over 50 million people with addictions globally.

Financial Benefits

Quitting smoking not only improves health but can also help your wallet. On average cigarette consumption is around 10 cigarettes a day among smokers in the UK and as of January 2024 the average price of a packet of 20 was more than £14, that is almost £50 per week, £196 per month and can be a staggering £2,352 on cigarettes per year.

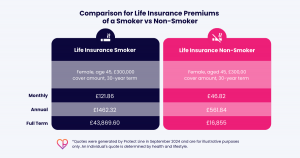

Smokers often pay higher life insurance premiums, sometimes more than double what they could be paying if they didn’t smoke. If you’ve been smoke-free for at least 12 months, some insurers may allow you to switch to non-smoking premiums, potentially saving you a significant amount of money.

Below is a comparison for life insurance premiums of a smoker vs non-smoker:

*Quotes were generated by Protect Line in September 2024 and are for illustrative purposes only. An individual’s quote is determined by health and lifestyle.

Could it be Time to Re-evaluate Your Policy?

Some insurers may allow you to adjust your premiums after being smoke-free for a year, though proof may be required in the form of a GP report, cotinine test or undergoing a chest x-ray. Check for any health changes since you took out your policy, as these could affect new or adjusted premiums. Be sure to compare quotes with a broker before making a decision, as other factors can also influence costs.

The Impact of Second-Hand Smoke

While life insurance companies currently do not ask about second-hand smoke, it’s important to remember that passive smoking is a serious health risk. It contains over 4,000 toxins, posing a threat even to those who do not smoke themselves. Although vaping does not produce smoke in the same way, research is ongoing regarding its effects.

New Year, New You

As you consider your resolutions for the New Year, remember that quitting smoking is a big step towards a healthier future. With health benefits and financial savings on the line, there’s never been a better time to make this life-changing decision.

And if you did quit smoking at the start of 2024, get in touch with us, you never know if you could be saving yourself some money with a new policy. Contact us today.

Critical illness plans may not cover all definitions of a critical illness. The definitions vary between product providers and will be described in the Key Features and Policy Document if you go ahead with a plan.

[1] GOV UK

[2] NHS

[3] GOV UK

Categories

Get a free life insurance quote today